Climate Blind Spots: Using Forward-Looking Cat Modeling to Address Rising Climate Risks - A Case Study

- Mar 23

- 7 min read

Turning Global Complexity into Strategic Certainty

NOTE: The below is only a snippet of the entire case study. If you would like to view/download the full case study, click below

EXECUTIVE SUMMARY

Aurelis Industrial Systems, a multinational manufacturer operating across 18 countries, identified a growing disconnect between stable historical loss performance and rising insurance costs.

While internal models suggested manageable exposure, insurers were pricing risk based on forward-looking climate volatility, revealing a critical blind spot in the company’s traditional, backward-looking catastrophe modeling approach.

A climate-adjusted, forward-looking risk assessment was undertaken, integrating hazard projections, geospatial exposure mapping, aggregation analysis, and financial stress testing. The review uncovered escalating flood risk at several facilities, increasing typhoon exposure in Southeast Asia, wildfire-related business interruption vulnerabilities, and portfolio-level aggregation risk exceeding internal tolerance thresholds.

Rather than waiting for losses or premium shocks, the company acted decisively — relocating a planned expansion site, investing in targeted mitigation, optimizing deductibles and limits, and strengthening insurer negotiations with data-driven insight.

As a result, projected earnings volatility declined, insurance pricing stabilized, and climate risk was elevated to a board-level strategic priority. The organization shifted from reactive risk management to integrated risk intelligence, effectively embedding forward-looking analysis into operational, financial, and capital planning decisions.

This case study underscores a critical reality: in an era of accelerating climate uncertainty, resilience depends not on historical averages, but on proactive, predictive risk insight.

CASE STUDY OVERVIEW

The Context

Aurelis Industrial Systems is a vertically integrated manufacturer specializing in engineered industrial components and automated material handling systems.

The company operates advanced manufacturing facilities, regional assembly centers, and strategically-positioned distribution hubs to an effort to support global supply chains in construction, energy, infrastructure, and heavy equipment.

The Situation

Aurelis Industrial Systems is a multinational industrial group operating in over 40 locations worldwide.

The organization’s footprint includes coastal production plants, inland logistics centers, and facilities located within rapidly expanding industrial corridors. Several sites are positioned in historically stable zones, but are becoming increasingly exposed to secondary perils, supply chain interdependencies, and evolving climate patterns.

Presently, their risk management effort have been structured based on:

Historical loss performance as the primary benchmark

Traditional catastrophe modeling calibrated to past event data

100-year floodplain maps as the standard measure of flood exposure

Annual renewal analytics focused primarily on premium trend and market capacity

For years, this framework appeared sufficient. Loss experience was manageable. Engineering reports were favorable. Insurance renewals, while sometimes firm, remained predictable.

Yet premiums continued to rise; driven by global insured loss trends, climate-adjusted underwriting assumptions, inflationary rebuilding costs, and shifting carrier appetite.

Internally, leadership maintained that the company’s exposure profile had not materially changed. No major acquisitions. No dramatic asset relocation. No meaningful deterioration in loss history. From an operational standpoint, the company’s exposure risks appeared stable.

From the insurance market’s standpoint, however, it did not.

The disconnect began to surface in board-level discussions, where directors grew concerned about the acceleration in volatility, capital allocation, and the long-term success predictability of the company’s property program as a whole.

The board then asked a critical question:

“Are we pricing today’s risks, or tomorrow’s?”

The Blind Spot

For decades, the company’s property program relied on traditional catastrophe modeling — heavily anchored in backward-looking loss history and static hazard assumptions. This approach provided a level of comfort: premium trends were predictable, loss experience was manageable, and facilities were largely considered moderate risk.

Yet beneath the surface, exposures were quietly evolving and in order for the company to find the gaps in their risk management processes, they needed to determine whether or not their existing risk analysis practices were still effective.

Table 1: Existing Risk Procedures - Findings & Conclusion

The Intervention

To address these blind spots, the organization performed a climate-adjusted, forward-looking catastrophe modeling review. This approach combined scenario planning, geospatial analytics, and financial stress testing to quantify emerging risks across the global portfolio.

The Findings

The analysis revealed several unexpected insights that challenged conventional risk assumptions:

Flood risk escalation

Typhoon exposure in southeast Asia

Wildfire-related Business Interruption

Aggregated Forward-Modeled Losses

The overarching insight was unmistakable: Traditional risk models, which rely heavily on historical loss data, consistently underestimate the scale and velocity of future uncertainty.

While past losses provide a baseline for understanding what has happened, they offer little guidance on what may come, especially as environmental and operational threats evolve at an accelerating pace.

Climate change, geopolitical volatility, and shifting supply chain dynamics introduce layers of risk that historical data alone cannot capture.

Organizations that leverage forward-looking intelligence using predictive modeling, scenario analysis, and emerging hazard data can identify vulnerabilities before they materialize.

By anticipating these exposures, they are better positioned to implement targeted mitigation strategies, strengthen resilience, and make strategic decisions proactively, rather than being forced into reactive crisis management when unforeseen events occur.

In essence, the gap between traditional risk assessment and forward-looking insight represents both a challenge and a critical opportunity for organizations seeking to safeguard operations, assets, and long-term stability.

Strategic Actions

Rather than waiting for a catastrophic event or insurance-driven premium spike, the company took proactive measures to close the gaps and reveal all climate-driven blind spots:

Relocated one planned expansion site to lower projected hazard exposure

Invested in flood mitigation for two high-risk facilities

Adjusted deductibles to manage smaller losses and control cash flow

Increased coverage limits to address modeled aggregation risk

Leveraged modeling insights in insurer negotiations to secure better terms and demonstrate risk awareness

The Outcome

The interventions produced measurable enterprise benefits, including:

Reduced projected 10-year earnings volatility by actively managing risk concentration

Stabilized property insurance pricing trajectory, mitigating unexpected premiums spikes

Improved underwriting transparency with carriers, strengthening strategic partnerships

Elevated climate resilience to a board-level initiative, embedding risk intelligence into long-term planning

Most importantly, the company shifted from a reactive posture (responding to market signals, losses, or insurance-driven changes) to an active role in shaping its own risk profile. This transformation positioned the organization not just to survive emerging threats, but to strategically leverage risk engineering and intelligence as a competitive advantage in operational planning, capital allocation, and corporate resilience.

CASE STUDY TAKEAWAY

Climate risk is no longer a distant or theoretical concern; it is a present and accelerating force reshaping global property portfolios.

Traditional backward-looking approaches leave organizations exposed to emerging volatility, hidden accumulation, and misaligned insurance structures. By integrating forward-looking catastrophe modeling, organizations can move beyond reactive risk transfer toward proactive portfolio design, gaining clearer visibility into climate-driven loss potential, capital adequacy, and geographic vulnerability.

The outcome is not only improved resilience and more informed underwriting engagement, but also a stronger ability to anticipate pricing shifts, optimize limits, and prioritize mitigation investments where they matter most.

To support decision-making and executive alignment, the following graphics provide a simple breakdown of the most important components of this evolution and effectively translating complex climate intelligence into clear, actionable insights that guide a more adaptive and future-ready global property strategy.

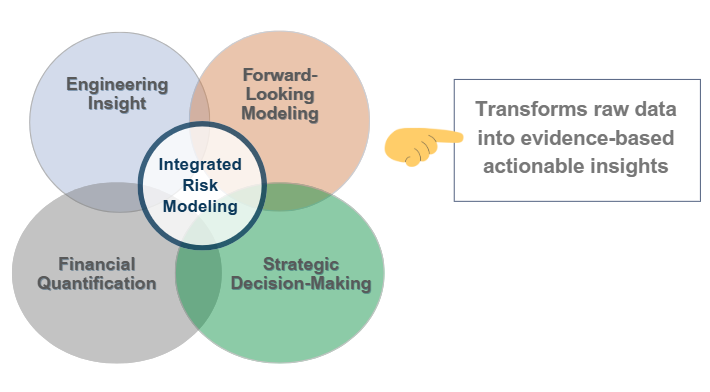

At the foundation, the risk intelligence lifecycle has three main elements:

Forward-looking modeling expands insight from what is known to what is plausible and prevents insight from being backward-looking and creates decision foresight, while financial quantification (i.e.: translating risk into business language) is where insight becomes actionable and converts technical understanding to economic relevance. Only when risk is technically understood, probabilistically explored, and financially translated can leadership confidently; this is where insight converts to organizational behaviour.

The graphic below provides a structured view of climate risk dimensions to support informed strategic responses. When analyzing risk, specifically in relation to climate-driven exposures, remember this:

Aurelis Industrial Systems’ experience demonstrates a defining shift in modern risk management: climate risk can no longer be measured based off of what’s happened in the past - climate risks must be managed by using data and foresight to predict what could happen in the future.

By challenging its reliance on backward-looking catastrophe models and historical averages, the company uncovered emerging exposures that were already influencing insurance pricing and long-term volatility. Forward-looking climate modeling revealed escalating secondary perils, hidden flood vulnerabilities, supply chain interdependencies, and aggregation risks that traditional frameworks failed to capture.

Through integrated climate mapping, asset-level exposure analysis, and financial stress testing, Aurelis translated complex hazard projections into quantifiable earnings-at-risk and capital impact scenarios. This enabled leadership to move decisively by relocating expansion plans, investing in targeted mitigation, optimizing deductibles and limits, and strengthening insurer engagement with data-driven transparency.

The result was not merely improved insurance outcomes, but a structural transformation in governance and decision-making. Risk intelligence became embedded in capital allocation, operational planning, and board-level strategy. Earnings volatility was reduced, insurance pricing stabilized, and resilience enhanced across the company’s entire global portfolio.

Ultimately, this case study reinforces a critical insight: organizations that integrate engineering expertise, predictive modeling, and financial quantification into a unified risk intelligence framework position themselves to anticipate volatility rather than absorb it. In an era of accelerating climate uncertainty, proactive foresight — not reactive response — defines sustainable resilience and long-term competitive strength.

--------

Wilson M. Beck Global Risks brings this expertise to organizations operating across borders. With a dedicated focus on complex multinational risk, WMB Global Risks supports clients through every phase of global program design, implementation, and ongoing stewardship.

By combining strategic oversight with local market insight, WMB ensures not only compliance and efficiency, but also alignment with an organization’s broader risk management objectives to deliver consistent protection, clarity at claims handling, and confidence in an increasingly complex and uncertain landscape.

To download the full case study, click below

Get the WMB Difference

Need Help?

Contact Wilson M. Beck Global Risks to discuss how to protect your business - wherever it takes you.

Wilson M. Beck Global Risks Inc. is a boutique division of Wilson M. Beck Insurance Services, offering tailored insurance and risk management solutions backed by over 100 years of combined experience.

Our team delivers personalized service rooted in trust, collaboration, and genuine care, ensuring every client feels understood, supported, and confident in their protection.

Our specialization in multinational insurance and corporate risk solutions is designed for mid-sized to large organizations that demand personalized service, specialized expertise, and seamless execution – wherever your business grows.

Contact Wilson M. Beck Global Risks to find out more about how our team of global experts can protect your operations and help keep you resilient, compliant, and in business.

We Care. We Help.

Comments